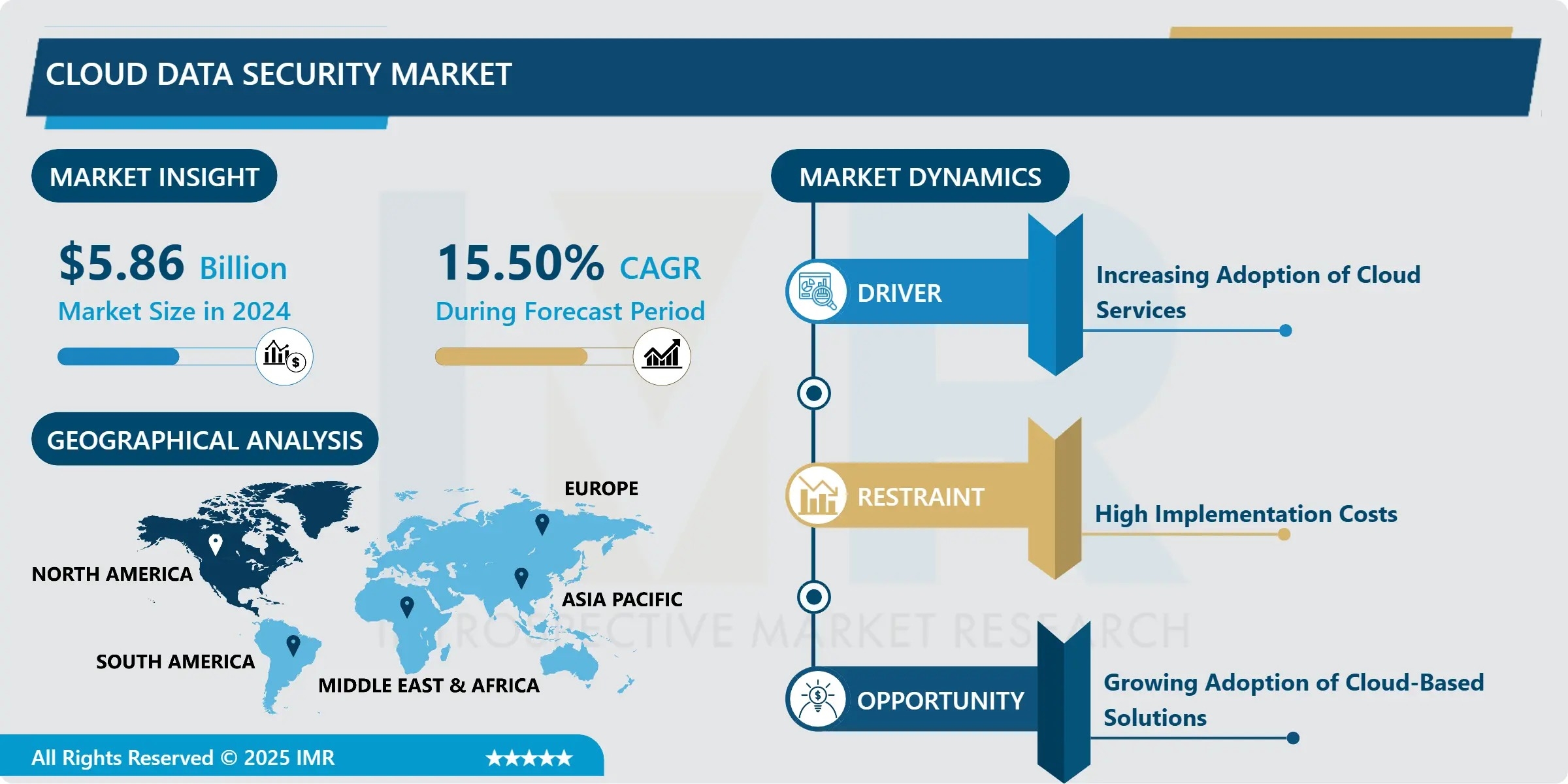

According to a new report published by Introspective Market Research, the Global Cloud Data Security Market by Component, Deployment, Organization Size, and Vertical, valued at USD 5.86 Billion in 2024, is projected to reach USD 18.56 Billion by 2032, growing at an exceptional CAGR of 15.50% from 2025 to 2032. This explosive growth is fueled by the massive migration of business-critical data to cloud environments, escalating sophistication of cyber threats, and the global proliferation of stringent data privacy regulations that mandate robust protection for data across hybrid and multi-cloud infrastructures.

Cloud Data Security encompasses specialized tools, policies, and controls designed to protect data stored, processed, and transmitted within cloud computing environments. Unlike traditional on-premises security, these solutions are built for the dynamic, distributed nature of the cloud, offering advantages such as scalability, centralized policy management, and deep integration with cloud service provider (CSP) platforms. They provide comprehensive protection through data discovery & classification, encryption, tokenization, access governance, and threat detection specifically tuned for cloud data stores like object storage, databases, and SaaS applications, ensuring confidentiality, integrity, and availability as data moves beyond the corporate perimeter.

A Key Growth Driver: The Unrelenting Migration to Cloud and SaaS, Coupled with Regulatory Scrutiny

A primary driver propelling the cloud data security market is the unstoppable enterprise transition to cloud infrastructure and Software-as-a-Service (SaaS) applications, combined with intense regulatory scrutiny of data handling practices. As organizations move sensitive workloads and customer data to platforms like AWS, Azure, and Google Cloud, and adopt SaaS tools like Salesforce and Microsoft 365, their security perimeter dissolves. This creates unprecedented visibility and control challenges. Simultaneously, regulations like GDPR and CCPA hold data controllers responsible for breaches regardless of where data resides—on-premises or in the cloud. This dual pressure forces organizations to invest in cloud-native security tools that can discover shadow IT, encrypt data, monitor user activity, and generate audit trails to prove compliance in complex, multi-cloud environments.

A Key Market Opportunity: The Rise of AI-Powered Data Security Posture Management (DSPM) and Automation

A transformative market opportunity lies in the development and adoption of AI-driven Data Security Posture Management (DSPM) platforms that automate risk identification and remediation. Traditional tools often generate overwhelming alerts. Next-generation DSPM solutions use machine learning and behavioral analytics to continuously map an organization's entire cloud data estate, automatically classify sensitive data, identify misconfigurations (e.g., publicly accessible storage buckets), detect anomalous access patterns, and prioritize risks based on context and potential impact. Furthermore, they can automate remediation workflows, such as applying encryption or adjusting access policies. Vendors that can deliver intelligent, automated platforms that reduce the burden on security teams while improving overall security posture will capture dominant market share as data volumes and cloud complexity continue to surge.

The Cloud Data Security Market is segmented on the basis of Component, Deployment, Organization Size, and Vertical.

Vertical

The Vertical segment is further classified into BFSI, Healthcare, Retail & E-commerce, IT & Telecom, Government, and Others. Among these, the BFSI (Banking, Financial Services & Insurance) sub-segment accounted for the highest market share in 2024. Financial institutions are at the forefront of cloud adoption for agility and innovation but handle the most regulated and attractive data for attackers. Their need to secure customer financial data, transaction records, and intellectual property in the cloud, while complying with strict mandates (GLBA, SOX, PCI-DSS), makes them the largest and most sophisticated consumers of comprehensive cloud data security solutions, driving significant investment in encryption, CASB, and advanced threat detection.

Organization Size

The Organization Size segment is further classified into Large Enterprises and Small & Medium Enterprises (SMEs). Among these, Large Enterprises accounted for the highest market share in 2024 due to their vast, complex multi-cloud deployments and substantial security budgets. However, the Small & Medium Enterprises (SMEs) sub-segment is projected to exhibit the highest CAGR. SMEs are increasingly targeted and are adopting cloud services at a rapid pace. The growing availability of affordable, cloud-delivered security-as-a-service models and managed security service providers (MSSPs) tailored for SMEs is democratizing access to enterprise-grade protection, fueling accelerated growth in this segment.

Some of The Leading/Active Market Players Are:

- Palo Alto Networks, Inc. (USA)

- Microsoft Corporation (USA) - (Microsoft Purview, Defender for Cloud)

- Broadcom, Inc. (Symantec) (USA)

- Cisco Systems, Inc. (USA)

- IBM Corporation (USA)

- Check Point Software Technologies Ltd. (Israel)

- Fortinet, Inc. (USA)

- Zscaler, Inc. (USA)

- McAfee, LLC (USA)

- CrowdStrike Holdings, Inc. (USA)

- Trend Micro Incorporated (Japan)

- Forcepoint (USA)

- Netskope (USA)

- Proofpoint, Inc. (USA)

- Lookout, Inc. (USA)

and other active players.

Key Industry Developments

News 1: Strategic Platform Consolidation Through Major Acquisition

In October 2024, Palo Alto Networks announced the acquisition of a leading Cloud Data Security Posture Management (CDSPM) startup. The integration aims to combine the startup's advanced data discovery and risk prioritization engine with Palo Alto's Prisma Cloud platform to create a unified cloud-native security offering.

This acquisition underscores the industry trend toward platform consolidation. Security leaders are seeking to provide customers with a single, integrated platform for all cloud security needs from network and workload security to comprehensive data security simplifying management and improving efficacy.

News 2: Launch of Generative AI Data Security Module

In July 2024, a major cybersecurity firm launched a dedicated security module designed to protect sensitive enterprise data within Generative AI applications and large language model (LLM) platforms. The solution focuses on preventing data leakage, ensuring compliance, and managing AI-specific risks.

This innovation highlights how the market is rapidly evolving to address new frontiers of risk. As enterprises adopt Generative AI tools that process vast amounts of data, specialized security controls are required to govern data flow, monitor prompts/responses, and prevent the exposure of sensitive information, creating a new high-growth niche within cloud data security.

Key Findings of the Study

- The BFSIvertical and Large Enterprises organization size segment dominate current market revenue.

- North Americais the largest regional market, while Asia-Pacific is projected to grow at the highest CAGR, driven by digital transformation and cloud adoption.

- Key growth is fueled by accelerated cloud migration, stringent data privacy laws, and the increasing sophistication of cyber threats targeting cloud data.

- Major trends include the convergence into unified Cloud-Native Application Protection Platforms (CNAPP) and the integration of AI for automated threat detection and posture management.

- The market is highly competitive, featuring pure-play cloud security vendors, traditional network security giants expanding their portfolios, and cloud providers offering native tools.