The cost of healthcare keeps increasing annually, and a lot of families are under pressure. Medical expenses may easily impact your monthly budget, whether it is a doctor visit or a prescription. A Health Savings Account, also referred to as an HSA, is one of the most intelligent tools at present. When used correctly, it offers powerful HSA tax advantages that can reduce your total healthcare costs and even support your long-term financial goals.

The great majority of people open an HSA without realizing the extent of its value. Before making decisions, it is often helpful to speak with a healthcare tax professional who understands how these accounts work alongside your income, insurance plan, and tax situation. With the right guidance, you can unlock the full potential of the HSA tax advantages available to you.

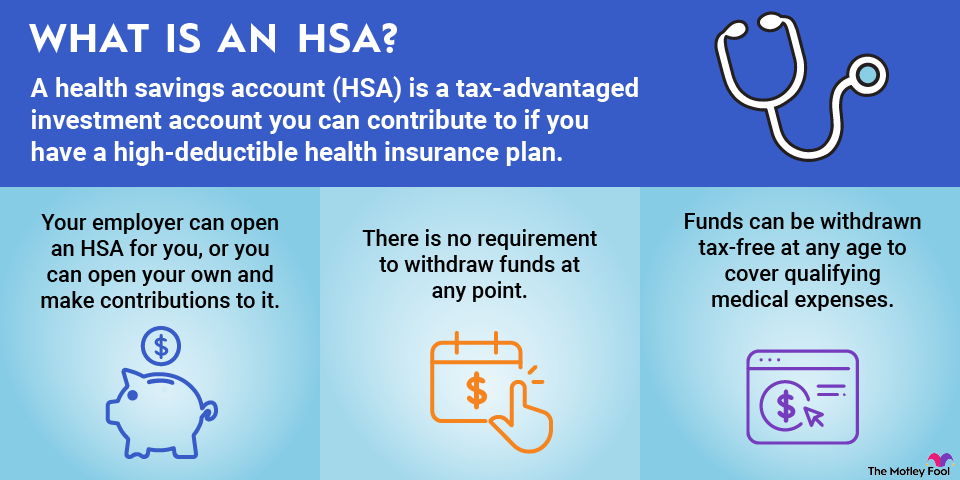

The Basics of an HSA

A Health Savings Account is an opportunity that is offered to people who are enrolled in a high-deductible plan. You deposit money in the account, and that money can be utilized on qualified healthcare services like doctor visits, dental treatment, medication, and even a few vision treatments.

The difference between HSAs and any other savings account is their tax treatment. The contributions are made using pre-tax dollars, and this implies that the money is deposited in the account before the income tax is charged. The savings may then increase over time by interest or returns on an investment, depending on the setup of the account.

The true power of HSA tax advantages lies in what experts often call the triple tax benefit. First, your donations lower your taxable income. Second, the money increases free of tax. Third, as you take money to pay qualified medical expenses, you are not subject to taxation on the money you take. This type of structure is hardly available in financial tools.

The Reduction of Your Taxable Income

Among the immediate advantages of making contributions to an HSA is the tax reduction in taxable income. When you make the maximum contribution that you can make within the year, the contribution is deducted from your income prior to the calculation of taxes. This is capable of reducing the amount of taxes that you pay at the year-end.

These HSA tax advantages are especially helpful for families who expect regular medical expenses. You spend the money that has never been taxed in the first place to pay the bills using after-tax money.

Long-Term Growth and Retirement Planning

The most common understanding of an HSA is that it is merely a short-term account used for medical spending; however, it is not always a potent tool. The money will roll over to the next year if you do not spend the entire amount of money within a particular year. It has no time limit to spend.

Certain HSA insurance companies also enable you to invest your balance in mutual funds or other investment plans after attaining a specific value. This implies that your account may increase over a number of years, like a retirement account. At a later age, particularly after sixty-five years of age, you can utilize the money to cover medical expenses without paying taxes. You can even take out the money on non-medical grounds after that age, but in such a case, taxes are likely to be paid.

When planned properly, these HSA tax advantages can help cover healthcare costs during retirement, which is often one of the largest expenses people face after leaving the workforce.

Using Your HSA Wisely

In order to maximize your account, it is worthwhile to know what falls under the allowable expenses. Visits to doctors, hospital treatment, medications, mental health services, and numerous preventive interventions are included. It is always good to keep good records and receipts so that in case you need to understand how the money was spent.

Another important factor is to contribute regularly, when possible, in case of a budget. Even a little donation every month can work wonders. Reviewing your strategy each year with a healthcare tax professional[1] can ensure that you are staying within contribution limits and making decisions that fit your overall financial plan.

Why HSAs Are Still Gaining Popularity?

As the cost of healthcare is rising, employers are increasingly providing high-deductible plans with HSAs. People are coming to the realization that these are not simply accounts of paying medical bills. They are concerned about the establishment of a financial cushion.

HSAs are unique because of their tax savings, long-term growth, and flexibility. When compared to traditional savings accounts or even some retirement options, the HSA tax advantages stand out clearly. If you want to gather more tax advantages, you must consult a Certified public accountant in Richardson. They provide the best and professional tax services along with expert financial management.

Conclusion

Cost reduction in healthcare is not merely in seeking cheaper services. It is concerning the application of intelligent financial tools. With proper management, a Health Savings Account will not only decrease the taxable income but will also expand savings and equip you with funds for future medical needs. Knowledge of the regulations and consultation of the appropriate guidance, where it is necessary, can turn daily spending on healthcare into a financial key benefit.

References:

[1] https://hmtaxgroup.com/practice-areas/healthcare-tax-services